COLLINS ACQUISITION MORE THAN DOUBLES TRADEHOLD’S SIZE

Tradehold’s acquisition of the KZN-based Collins Group towards the end of its February 2017 financial year has more than doubled its balance sheet. By 31 August 2017 total assets had grown to £994 million – 161.7% higher than the £380 million at the end of the corresponding period in 2016. Shareholder equity has risen 74.8% to £306.8 while revenue has increased 165.5% to £55.5 million (2016: £20.9 million). Headline earnings per share were up 169% compared to the corresponding six months.

Although the major part of its gross assets are now in South Africa, Tradehold continues to report its results in pound sterling as the operations of most of its subsidiaries are still conducted in that currency.

Total profit for the period attributable to shareholders stood at £10.8 million while tangible net asset value, calculated by management to exclude goodwill and deferred tax, was 54.8% higher at 134.2 pence per share.

Tradehold joint CEO Friedrich Esterhuyse said the acquisition of Collins, a fourth-generation family business, had provided the company with an extremely solid, well established base from which to grow its operations in South Africa.

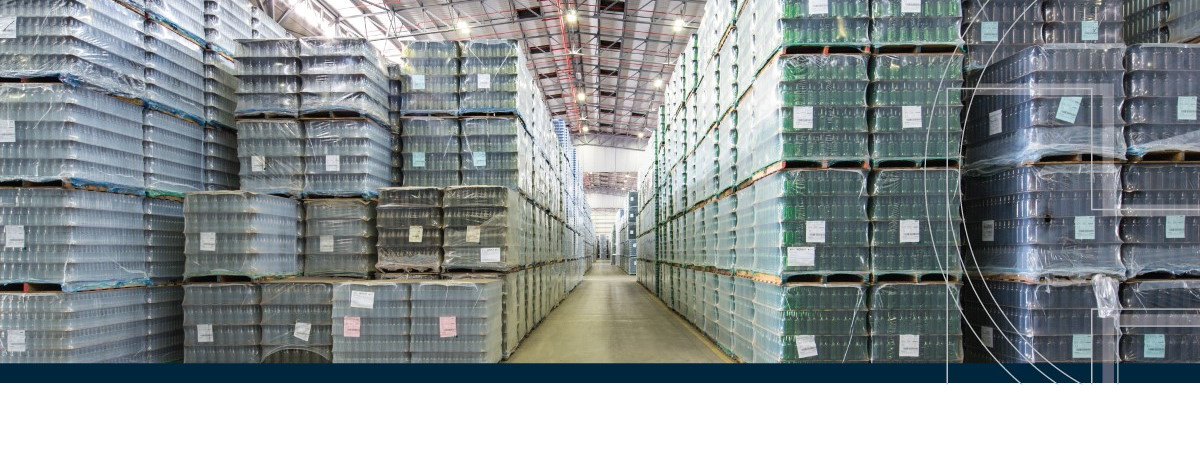

“Collins owns a portfolio 152 mainly industrial properties that has a gross lettable area (GLA) of 1,6 million m² and include large state-of-the-art distribution centres and major industrial complexes that are let on long-term triple net leases to tenants such as Unilever, Sasol, Massmart, Nampak and Pep. Retail represents about 6% of the portfolio, with tenants such as Shoprite, Pick n Pay, Edcon and Boxer, with the remaining 3% being office space. GLA occupancy was 98,6% for the period.”

Tradehold operates in two main markets, the UK and South Africa. It does, however, also have investments elsewhere in Southern Africa, as well as in financial services. Towards the end of the reporting period Tradehold announced that it was stripping out its financial services division and listing it in a separate company, a process which is expected to be completed towards the end of the financial year.

During the reporting period, Tradehold enjoyed solid growth in the UK where it owns 100% of the Moorgarth group. The latter in turn owns a substantial property portfolio which includes London office buildings and several retail malls, all of them strategically located in densely populated areas with a high levels of passing trade. In the six months to August, it increased the value of its portfolio to £177 million (or to £234 million if its interest in joint ventures is included). Moorgarth generated turnover of £13,7 million.

By continuously expanding its offering of serviced office space through its wholly-owned subsidiary, London-based The Boutique Workplace Company (TBWC), Moorgarth has been able to capitalise on changing market dynamics, with companies increasingly hesitant to enter into long-term leases or to invest in infrastructure of their own. TWBC grew turnover by 12% to £8.5 million.

After the end of the reporting period Moorgarth acquired a further two centrally located buildings in London, to be refurbished to fit the needs of TBWC.

Tradehold Africa increased the value of its portfolio to £lI9.4 million. The main focus of its operations continued to be on Namibia where one of its major retail developments, the 27 000m² Dunes Mall in Walvis Bay in partnership with Atterbury Property Group, was recently completed at a cost of £29 million.

Esterhuyse said Tradehold had made considerable progress with its plan to list its Namibian interests on the Namibian Stock Exchange. Discussions with key investors were under way and, if successful, would result in a listing by the end of the 2018 financial year.

Tradehold chairman Christo Wiese said although the political volatility and economic instability in the UK and South Africa offered considerable challenges, he believed management had shown itself more than capable of navigating its way around them.

“In fact, I believe our results for the past reporting period amply show the extent of management's capacity to respond entrepreneurially and deliver solid growth even under these circumstances,” Wiese said.

Commenting on Tradehold’s decision to strip out its financial services division and listing it in a separate company, Esterhuyse said the simplified group structure should make it easier for investors to value the two individual businesses in terms of the potential they offered. “In the case of Tradehold’s property interests, I trust a clearer understanding of the potential and opportunities they present will narrow the discount between tangible net asset value and current market capitalisation.

“If one assumes that its South African industrial portfolio should trade at close to tangible net asset value, as is the case with similar businesses listed on the JSE, then the discount to TNAV attributed to the balance of the portfolio, which is predominantly UK based, is around 50%. This seems excessive given our strategy in the UK of acquiring only assets with the potential of enhancing capital value through active management.

”Which implies that, in my view, the company’s shares at present offer considerable upside for investors,” Esterhuyse said.

ISSUED BY Tradehold Ltd

DATE ISSUED

9 November 2017

MEDIA ENQUIRIES

Friedrich Esterhuyse, joint CEO, Tradehold

021 928 4800